Category: Uncategorized

-

Nvidia CEO says selloff in tech stocks is a buying opportunity

Nvidia Corp. chief executive Jensen Huang called a global tech stocks selloff that began last week a buying opportunity, saying the buildout of artificial intelligence has just begun.

South Korea’s benchmark Kospi Index tumbled on Monday after investors pulled back from AI bets that have fueled a bull market in global equities. Fears of overheating in the AI trade have cooled global tech stocks, with U.S. peers tumbling Friday on concerns over a possible rate hike.

Huang, responding to questions about how that selloff should be perceived, said the industry was still in the early stages of constructing infrastructure that will serve as the foundation of an AI-fueled future. On Monday, Nvidia and SK Hynix Inc. said they struck a multi-year agreement to design future generations of memory chips for AI, a win for a South Korean leader vying with Samsung Electronics Co. in the red-hot arena. Stocks including SK Hynix pared losses after South Korean President Lee Jae Myung said Monday he believed the domestic market remained undervalued.

Article content

“We’re at the beginning of it, and whatever happened to the stock market, you should be very happy because now you can buy at a discount,” he said. “Everybody should be very excited,” he told reporters after meeting with SK Group Chairman Chey Tae-won in Seoul.

Article content

Like many of his industry peers, Huang has consistently argued that AI will revolutionize broad swaths of the global economy and transform the way people work and live. That will in turn drive huge demand for the data centers — and chips — needed to power future AI services.

Article content

“It is a foregone conclusion that AI will be infrastructure for the world, just like the internet was infrastructure for the world,” he said.

-

Canada’s business productivity falls for second straight quarter

One of the economy’s most persistent challenges reared its head again as rising labour costs outpaced growth at the start of 2026 and Canadian business productivity fell for the second straight quarter.

Article content

Statistics Canada said Wednesday a “mild contraction” in the pace of output reduced labour productivity in the business sector by 0.5 per cent in the first quarter, following a 0.3 per cent decrease in the fourth quarter of 2025.

The first-quarter decline was led by a contraction in goods-producing businesses, where productivity fell 1.7 per cent. The agriculture, forestry, fishing and hunting sector was the main contributor with a 3.5 per cent decline. Productivity also declined 1.3 per cent in the construction industry and 0.3 per cent in manufacturing.

Service-producing industries managed a modest 0.3 per cent increase. The strongest gains in productivity came from information and cultural industries (1.6 per cent), transportation and warehousing (1.2 per cent) and retail trade (one per cent).

“Overall, productivity decreased in 10 of the 16 main industry sectors in the first quarter,” the agency said.

Productivity, which measures the amount of economic output produced per hour worked, is widely viewed as a key measure of economic prosperity. Canada has struggled with weak productivity growth for decades and lags many peer countries, including the United States.

In a note, Desjardins economist LJ Valencia said real GDP in the Canadian business sector has fallen three times in the last five quarters as the ongoing trade tensions with Canada’s neighbour and largest trading partner continues to weigh on the economy.

Article content

Article content

“Looking ahead, our analysis suggests that the federal government’s immigration policies are expected to further slow population growth,” he said. “Still, uncertainty surrounding the trade war will shape the near-term trajectory of Canadian business investment and productivity, with the outcome of this year’s Canada–United States–Mexico Agreement (CUSMA) joint review being pivotal.”

As productivity dipped, overall hours worked rose 0.4 per cent, reflecting a 0.1 per cent rise in the number of jobs. Average hours worked also increased 0.3 per cent.

Article content

Meanwhile, labour costs continued to rise for the fourth quarter in a row. Hourly compensation went up 0.9 per cent, pushing unit labour costs (ULCs) up 1.4 per cent. According to Statistics Canada, ULCs measure the amount businesses pay in wages and benefits to produce one unit of real output.

Article content

“The acceleration of ULC growth in the beginning of 2026 is a worrying sign, as elevated costs continue to undermine Canada’s competitive position and continues to exacerbate challenges for businesses across the

-

Wall Street’s week ahead: Blockbuster SpaceX IPO set to test high-flying U.S. stocks rally

The long-awaited, massive SpaceX initial public offering is expected next week, a major event for the U.S. stock market, with investors wary of possible overexuberance.

Stock indexes fell on Friday as strong jobs data ignited fears of hawkish monetary policy and semiconductor shares tumbled after a torrid run. The benchmark S&P 500 posted a weekly decline after nine straight weeks of gains.

The S&P 500 was still up about 8% in 2026, including a 16% rebound since its late-March low for the year.

“Nothing has stuck in terms of pessimism in the last two months,” said Mark Hackett, chief market strategist for Nationwide. “There is just this underpinning of momentum, this insatiable appetite for tech holdings and just the technical buying spree that is really dwarfing almost all other inputs.”

Next week, investors will also assess fresh data on consumer and producer prices, after the jobs report fueled fears that the Federal Reserve would focus on calming inflation, potentially leading to interest rate hikes. The coming week also brings earnings reports from key companies in the technology sector, which has driven the market’s recent surge despite a sour end to the week.

Some investors have been bracing for a pause, if not a pullback, after the sharp rally. Risks include the U.S.-Israeli war with Iran and the potential for renewed spikes in energy prices if Middle East tensions flare.

Elon Musk’s SpaceX is aiming to raise $75 billion, the most ever for an IPO, in a deal that would value it at $1.75 trillion. Pricing is expected on June 11, with trading to begin on the Nasdaq the next day.

The company has an unusual and diverse set of businesses, including rockets, satellite communications and AI computing. Adding in the involvement of Musk — Tesla’s leader and the world’s wealthiest man — and SpaceX’s valuation is tricky to pin down, rising to exorbitant levels by some measures. The company posted a net loss of $4.94 billion in 2025, even as revenue rose 33% to $18.67 billion.

The IPO could lure significant attention from retail investors and provide another high-profile way to gain exposure to the AI trade.

“We’ve got one of the biggest IPOs in history coming … which I think is the focus of everybody’s interest,” said Jason Pride, chief of investment strategy and research at Glenmede. “The question mark surrounding it is whether it’s an indication of market froth.” SpaceX’s debut is expected to be followed by other mega IPOs in the coming months from Anthropic and OpenAI, two of the AI leaders. Anthropic, which makes the Claude chatbot, said this week it has confidentially filed for a U.S. IPO.

The SpaceX IPO is “an important benchmark,” said Matt Wittmer, a portfolio manager at Allspring Global Investments, adding that “the company itself will be playing in some of those key areas that people are looking for to find new secular growth opportunities.”

The May Consumer Price Index, due on Wednesday, will show how surging oil and gasoline prices are influencing inflation. One concern is the extent to which higher energy prices might be affecting other CPI components, Pride said, ahead of the Federal Reserve’s meeting this month.

“The Federal Reserve is going to be watching this like a hawk,” Pride said. “They’re going to want to see those pieces continue to remain stable and not increase as a pass-through from the energy and food prices.”

In the wake of the spike in energy prices, futures are factoring in a greater chance the Fed raises interest rates this year rather than cuts, after markets had anticipated equity-friendly rate decreases at the start of 2026.

Other economic data next week includes Thursday’s report on producer prices. Quarterly reports from tech companies Oracle and Adobe will also be in focus. Tech has long dominated the U.S. stock market, but the sector’s recent outperformance pushed it to more than 39% of the S&P 500’s market capitalization this week, its highest share on record. The results will test the strength of the tech trade and the rebound in the software industry, which was hit hard to start the year on concerns about AI disruptions. Shares of Oracle are up more than 9% this year, while Adobe is down 28%.

“Getting more data points from some of the AI value chain is going to be important,” Wittmer said.

-

PM Carney travelling to Ireland and France for G7 summit

Prime Minister Mark Carney is heading to Europe on Thursday, visiting Ireland and France for the G7 summit.

The summit is running from June 15 to June 17 in Evian-les-Bains and France says the focus will be on reducing global inequalities.

The summit was delayed by a day after U.S. President Donald Trump announced that the White House would host a UFC fight on June 14, which is Flag Day in the United States and Trump’s 80th birthday.

Fen Osler Hampson, an international affairs professor at Carleton University, told The Canadian Press the leaders will have to focus on “managing Trump” at the summit.

“The real discussions will be among the remaining G6 leaders when Trump isn’t in the room, in terms of how you deal with a president who is irascible, unpredictable and making life difficult for everyone,” he said, noting that the president has personally insulted several European leaders.

The government of France says priorities at the summit will include settling major geopolitical crises, including through G7 support to Ukraine, online protection for children, crime and “the new rules of play of global governance.”

However, Hampson said the official agenda generally doesn’t reflect what the key issues of discussion will be. He said those are likely to include conflict in the Middle East, energy security and U.S. tariffs.

Canada hosted the G7 summit in Kananaskis, Alta., last year. Trump left a day early due to the conflict in the Middle East.

The G7 includes Canada, France, the United States, Germany, Japan, the United Kingdom and Italy. The European Union also participates in talks, though the bloc isn’t counted in the group’s name.

Before the summit, Carney is making stops in Paris and Dublin, Ireland.

A news release from the Prime Minister’s Office says Carney and Macron will discuss deepening ties in sectors such as defence, artificial intelligence, quantum technologies and critical minerals.

Ireland, which has become a major centre for foreign investment and businesses, is set to assume the presidency of the Council of the European Union in July.

The PMO notes Carney’s visit will be the first official trip for a Canadian prime minister to Ireland in nearly a decade. Carney will meet with the Taoiseach of Ireland, Micheál Martin and Irish President Catherine Connolly as part of talks to deepen cultural and trade ties between the nations.

Carney met with 150 Irish business leaders in Ottawa last month. The embassy said on social media that the discussion focused on economic opportunities for the countries, innovation, investment and growth across sectors.

Bilateral merchandise trade between Canada and Ireland reached $6 billion in 2025. Canadian exports of $1.1 billion to Ireland were led by cereals and imports of $4.9 billion were led pharmaceutical products.

Trade between the countries is underpinned by the Canada-European Union Comprehensive Economic and Trade Agreement, known as CETA, which has been provisionally applied but has not yet been ratified by several states, including Ireland.

Martin met with Carney in Ottawa in September. At the time, he said Ireland would be ratifying the CETA deal. A joint statement from the leaders said they agreed on the importance of Ireland’s full ratification of the agreement by 2026.

The Irish Times reported late last month that the Irish government was set to approve new legislation to accelerate ratification of the trade deal to reduce the country’s reliance on the United States.

There are an estimated 4.5 million Canadians that have Irish ancestry, representing almost 15 per cent of the country’s population.

Carney also has deep ties to Ireland, with his grandparents immigrating from County Mayo in the early 1920s.

This report by The Canadian Press was first published June 7, 2026.

-

Is Canada’s economy in trouble? What the latest GDP and job numbers mean for you

OTTAWA — There was one word on the lips of many Canadians economists, politicians and journalists this past week: recession.

Recent economic data has painted a mixed picture of Canada’s economy, and some interpretations make the argument for a recession.

Here’s what you need to know about the state of Canada’s economy.

Why are people talking about a recession?

On May 29, Statistics Canada reported real gross domestic product figures for the first three months of the year.

The quarter-over-quarter change was so mild that StatCan considered it statistically flat, or no change in real GDP.

But when economists are gauging the health of the economy in a given quarter, they often annualize quarterly figures, which can magnify small positive or negative changes in the numbers.

The annualized change in real GDP was a 0.1 per cent decline, coming off a one per cent drop in the fourth quarter of last year.

That data triggered the recession talk.

What’s a technical recession?

Two quarters in a row of declining GDP is a bar used by some analysts to define a “technical” recession, though a number of economists consider the term unhelpful.

Appearing before a parliamentary committee on Monday, Bank of Canada senior deputy governor Carolyn Rogers warned MPs against putting too much stake in that definition.

“Simply the fact that you have to put the term ‘technical’ in front of it sort of tells you that you need to really look past that one indicator,” she said.

The more widely accepted but nebulous definition of a recession refers to a downturn where Canada’s economy is not just shrinking on a technical basis, but where that weakness is widespread through the economy.

Recessions are marked by job losses, households reining in spending and tough operating conditions for businesses across the economy.

“Two consecutive quarters of negative GDP growth, or contracting GDP, is necessary but not sufficient to call a recession in Canada or anywhere else,” said Randall Bartlett, deputy chief economist at Desjardins.

What are political leaders saying?

The federal Conservatives have seized on the latest GDP results, blaming Prime Minister Mark Carney and the Liberals for a “full-blown recession.”

In addition to stagnant GDP, Conservative Leader Pierre Poilievre and other MPs have pointed to rising food bank usage, consumer insolvencies and job losses in the first four months of the year to argue Carney’s policies have damaged the Canadian economy.

Liberals have meanwhile largely avoided using the word “recession” at all while defending their economic stewardship.

Carney acknowledged this week that the latest GDP figures show some “weakness,” though he noted positive trends like rising business investment in machinery and equipment are encouraging.

The prime minister argued that cuts to immigration and government spending are weighing on growth. He also said the work to pivot the economy away from reliance on the United States is going to take time to pay off, and economic data will be “uneven” while that unfolds.

Poilievre has accused Carney of ducking accountability over the state of the economy.

Who decides if we’re in a recession?

A recession is not declared by the federal government, the Bank of Canada or any officially designated body.

In Canadian economic circles, the traditional arbiter of a recession is the C.D. Howe Institute’s Business Cycle Council. It performs a similar function to the National Bureau of Economic Research in the United States.

The council weighed in on the recession question Friday morning, arguing it was too soon to use the label to describe the state of Canada’s economy.

Declines in the economy must be pronounced, pervasive and persistent to be considered a recession, the think tank noted. This current downturn doesn’t yet meet that bar, the Business Cycle Council determined.

StatCan’s May 29 GDP report also expects the economy rebounded in April, setting the second quarter up for a return to growth. A week later, the agency reported a surprise gain of 88,000 jobs for May, which many economists said should pour cold water on recession talk.

What even is GDP?

Gross domestic product refers to the total value of finished goods and services produced in a country over a given period. It’s broadly used as a gauge of the economy’s health.

StatCan said rising imports of gold and declining business investment were offset by higher household spending and firms stockpiling inventory, leaving first-quarter GDP flat compared to the previous three months.

Bartlett said recent data is “idiosyncratic” from historical trends as the economy adjusts to U.S. tariffs and shifting geopolitical tides.

He also said GDP is not a perfect measure of the economy and struggles with tracking services. It can be volatile, and StatCan revises it initial reports regularly before landing on final figures months or years down the road.

Bartlett said that’s another reason to use caution around the latest figures.

“To hang your hat on one number that could easily be revised in either direction, either up or down, I think we need to see what these subsequent revisions look like to this data before we’d ever be comfortable making a call on a recession,” he said.

Why does GDP matter?

While GDP might not be a perfect measure, Concordia University economics professor Moshe Lander argues it’s still worth tracking. He compares it to his mother measuring his height by notching a mark on the door frame as he grew up — it’s the trend that matters.

“Even though it’s constantly revised, even though its riddled with flaws, and even though there is noise, what you do tend to find is that a lot of the things that do matter to us are highly correlated with this imperfect measure,” Lander said.

Rising GDP tends to mean businesses are producing more effectively, allowing them to raise wages. A better economy also means more tax dollars are flowing up to federal and provincial governments, which in theory helps Ottawa and the provinces fund better services for Canadians.

Real GDP per capita — measuring output on a per person basis — is sometimes used as a stand-in to measure whether quality of life is improving in a country.

Canada’s growth in real GDP per capita has lagged the United States for years, though the metric was positive in the first quarter of 2026, partly reflecting a shrinking population.

But measures like GDP, inflation and the unemployment rate are broad aggregates for the health of an economy and don’t necessarily reflect an individual’s experiences.

Lander said that makes relying on any one indicator an even more perilous venture for policy-makers and individual households trying to make sense of the economy.

“We’re increasingly living in our microeconomic world, and GDP is fundamentally a macroeconomic variable. Because society is becoming a little more unequal, coming up with one number to try and describe that macro economy is becoming increasingly frustrating,” he said.

“So when we say then that we entered a recession, I think there’s a big pushback then from people saying, ‘Uh, I feel like I’ve been in a recession for the last decade.’”

This report by The Canadian Press was first published June 7, 2026.

-

Things To Look Out For: Week Ending June 12, 2026

Summary:

- TSX starts the week under pressure after closing June 5 at 34,413.45, down 2.28% on the day, following a broad risk-off sell-off.

- Wednesday, June 10 is the key day: U.S. CPI at 8:30 a.m. ET and the Bank of Canada rate decision at 9:45 a.m. ET.

- Rates and inflation are the main TSX drivers this week. Hot U.S. inflation would pressure tech, real estate, utilities and gold.

- Middle East / Strait of Hormuz risk remains critical for oil, energy stocks, gold and inflation expectations. Reuters reported global stocks fell and oil rose as hopes for a quick Iran-war resolution faded.

- Base case: volatile TSX, with energy supported by oil risk, while tech and rate-sensitive sectors stay vulnerable.

Key Events to Watch

Date Event TSX Impact Mon Jun 8 No major scheduled releases Market digests Friday sell-off; watch technical rebound or follow-through selling. Tue Jun 9 Canada merchandise trade balance; U.S. trade balance CAD, industrials, materials, exporters. Wed Jun 10 U.S. CPI — May Biggest global market risk. Hot CPI = higher yields, negative for tech/gold/REITs. Wed Jun 10 Bank of Canada rate decision Banks, CAD, utilities, real estate, consumer stocks. Thu Jun 11 U.S. PPI; Canada building permits; ECB meeting Inflation + housing + global rate tone. Fri Jun 12 U.S. Michigan sentiment; Canada capacity utilization Consumer confidence and industrial demand signals.

Sector Impact — TSX

Sector Bias This Week What to Watch Energy Positive / volatile Oil prices, Hormuz disruption, Iran-war headlines. Materials / Gold Mixed Gold may rebound if fear rises, but hot CPI / higher yields are negative. Financials Mixed BoC tone, yield curve, credit-risk language. Technology Negative bias U.S. Nasdaq weakness, bond yields, AI/semiconductor sell-off. Utilities / REITs Vulnerable Higher yields reduce valuation support. Consumer discretionary Vulnerable Inflation, rates, consumer sentiment. Staples Defensive Could outperform if risk-off continues.

Base / Bull / Bear Scenarios

Scenario Trigger Likely TSX Reaction Bull U.S. CPI softer than expected + BoC neutral/dovish + oil stable TSX rebound; tech, banks, rate-sensitive stocks recover. Base CPI near expectations + BoC holds steady + geopolitical risk contained Choppy, sideways TSX; sector rotation continues. Bear Hot CPI + hawkish BoC/Fed repricing + Middle East escalation TSX sells off further; tech, REITs, gold exposed; energy may outperform but volatility rises.

Actionable Takeaways

- Watch June 10 first: U.S. CPI and BoC are the week’s main market-moving events.

- For TSX direction, monitor U.S. 10-year yield, WTI oil, gold, CAD/USD and Nasdaq futures.

- Stronger inflation data likely favours energy and defensive sectors over tech and rate-sensitive stocks.

- A cooler inflation print could support a short-term rebound after Friday’s sell-off.

- Keep risk controls tight: this week is driven more by macro headlines than company fundamentals.

-

Calendar: June 8 – June 12

Monday June 8

China’s foreign reserves, aggregate yuan financing, new yuan loans and trade surplus

Japan’s real GDP and bank lending

Germany’s factory orders

(11 a.m. ET) U.S. New York Fed one-year inflation expectations

Earnings include: Campbell’s Co.

Tuesday June 9

Japan’s machine tool orders

Germany’s industrial production and trade surplus

(8:15 a.m. ET) U.S. ADP Employment (four-week average change).

(8:30 a.m. ET) Canada’s merchandise trade balance for April.

(8:30 a.m. ET) U.S. goods and services trade deficit for April.

(10 a.m. ET) U.S. existing home sales for May. The Street expects an annualized rate rise of 0.7 per cent.

(10 a.m. ET) U.S. wholesale inventories for April.

Earnings include: Casey’s General Stores Inc.; JM Smucker Co.; Stingray Group Inc.

Wednesday June 10

China’s CPI and PPI for May.

(8:30 a.m. ET) U.S. CPI for May. The Street is projecting a gain of 0.5 per cent from April and 4.2 per cent year-over-year.

(9:45 a.m. ET) Bank of Canada’s policy announcement with press conference to follow at 10:30 a.m.

(2 p.m. ET) U.S. budget balance for May.

Earnings include: Oracle Corp.; Major Drilling Group International Inc.; North West Co. Inc.

Thursday June 11

ECB’s monetary policy meeting

(8:30 a.m. ET) Canadian building permits for April. Estimate is a month-over-month decline of 3.0 per cent.

(8:30 a.m. ET) U.S. initial jobless claims for week of June 6. Estimate is 219,0000, up 6,000 from the previous week.

(8:30 a.m. ET) U.S. PPI Final Demand for May. Consensus is a rise of 0.7 per cent from April and up 6.4 per cent year-over-year.

(10 a.m. ET) U.S. quarterly services survey for Q1.

Earnings include: Adobe Systems Inc.; Dollarama Inc.; Lennar Corp.

Friday June 12

Japan’s industrial production

Germany’s CPI

(8:30 a.m. ET) Canada’s national balance sheet and financial flow accounts for Q1.

(8:30 a.m. ET) Canadian new motor vehicle sales for April. Estimate is a year-over-year fall of 5.0 per cent.

(10 a.m. ET) U.S. University of Michigan consumer sentiment survey for June (preliminary reading).

-

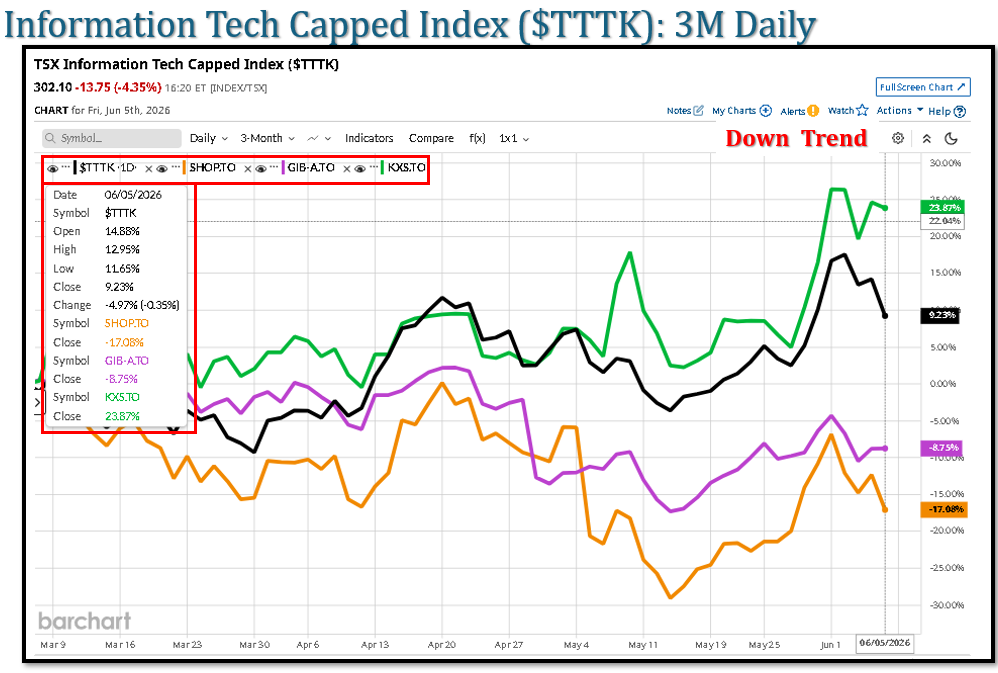

June 5- TTTK Performance

Executive Summary — TTTK.TO / S&P/TSX Capped Information Technology

- TTTK weakened over the past 5 trading days, mainly because TSX technology stocks sold off with North American growth/AI names.

- The sharpest pressure came Friday, June 5, when the TSX had its biggest drop in nearly four months and technology was one of the leading losing sectors.

- U.S. tech weakness spilled into Canada: the Nasdaq fell 4.18% Friday, with semiconductors and growth stocks hit by higher-rate concerns.

- Key TTTK constituents were weak on June 5: Shopify -5.42%, BlackBerry -9.17%, Lightspeed -2.43%, OpenText -1.95%, while CGI was flat.

- Cause: rate-hike / bond-yield pressure + risk-off selling after strong U.S. jobs data, which hurts long-duration tech valuations more than defensive sectors.

Brief explanation:

TTTK.TO fell because Canadian tech was caught in a broader North American tech sell-off. Strong U.S. employment data reduced expectations for rate cuts and raised concern that the Fed may stay hawkish or even hike later, pressuring high-valuation growth stocks. The move was amplified by weakness in major Canadian tech names such as Shopify and BlackBerry, while the broader TSX also sold off sharply on Friday.Bottom line: short-term move was mainly macro-driven multiple compression, not a sector-specific earnings collapse. A rebound would likely require lower bond yields, stabilization in U.S. tech/AI stocks, and recovery in Shopify/Constellation/Kinaxis-type leaders.